Global Fisheries and Aquaculture Outlook for 2024/2025: EFFOPs Analysis

2024.6.17

The Food and Agriculture Organization of the United Nations has released its Food Outlook report for the 2024/2025 period, providing a comprehensive analysis of global food commodities. According to the report, supplies of most major food commodities are expected to be adequate in 2024/2025. However, factors such as extreme weather, rising geopolitical tensions, sudden policy changes, and other variables could disrupt the delicate global demand-supply balances, potentially impacting prices and global food security. You can download the full report here

Production Overview

On the production front, the world is poised for record outputs in rice and oilseeds, while wheat and maize production are projected to decline modestly. The Food Outlook also includes FAO’s preliminary estimate for the global food import bill in 2024, forecasting a rise of 2.5% to surpass $2 trillion. This increase is driven by relatively favorable macroeconomic conditions, including steady global economic growth and lower food commodity prices.

Fisheries and Aquaculture Sector Analysis

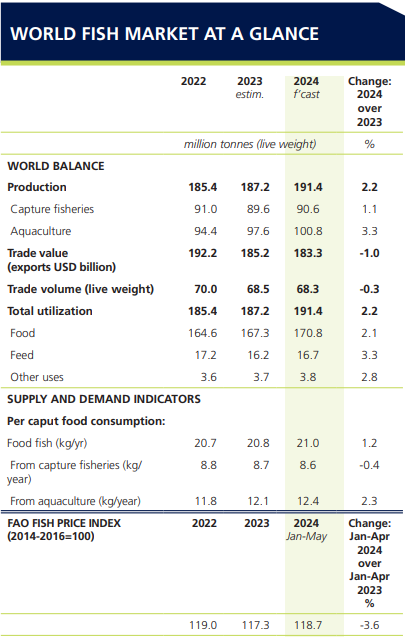

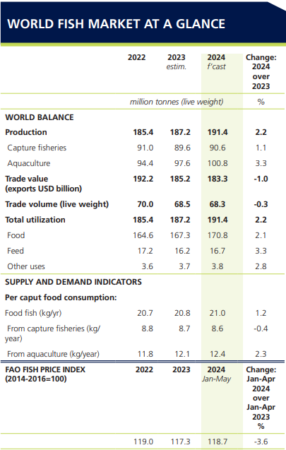

In the fisheries and aquaculture sector, 2024 is expected to see stable landings from capture fisheries alongside a robust expansion in aquaculture. In total, seafood production is anticipated to grow by 4.2 million tonnes, or 2.2%, reaching a total output of 191 million tonnes with 16.7 milion tonnes expected to be utilized for feed purposes representing a 3.3% increase from 2023. Aquaculture alone is also projected to grow by 3.3%, achieving 100.8 million tonnes. This growth is largely attributed to a surge in farmed shrimp production, along with smaller increases in oysters and carp. However, despite these gains, the sector continues to grapple with some challenges, including low market prices and high production costs. Overall demand remains withheld, which, coupled with an increased supply of certain aquaculture species, has led to a decrease in prices for some aquatic products. Rising production costs and stagnant consumer spending further complicate the market landscape.

Economic and Trade Implications

Global economic conditions have shown notable improvements, with lower inflation rates and stronger-than-expected GDP growth in some countries. However, consumer spending patterns in major markets such as the United States and the European Union remain notably restrained. This has been reflected in a sluggish demand for many segments of the aquatic food market, with consumers showing a preference for lower-priced seafood products. The value of global trade in aquatic animal products is expected to decline by 1.0% in 2024. Major importers such as China, the European Union, the United States, and Japan are all anticipated to see a contraction in trade value compared to the previous year. Trade volumes are projected to remain largely flat, with a slight decline of 0.3% from 2023 levels.

All in all, the 2024/2025 outlook for fisheries and aquaculture presents a mixed picture. While production is set to increase, the sector faces ongoing challenges from economic pressures and shifting consumer behavior. The global market for aquatic products will need to navigate these complexities to achieve sustainable growth and stability.