Agricultural commodity and fish markets outlook 2023-2032

2023.7.26

The Organisation for Economic Co-operation and Development (OECD) and the Food and Agricultural Organization (FAO) of the United Nations published on July 6, the latest edition of the OECD-FAO Agricultural Outlook. The report provides an assessment of the ten-year prospects for agricultural commodity and fish markets and highlights fundamental economic and social trends that drive the global agri-food sector, assuming there are no major changes to weather conditions or policies.

The fish chapter focuses on recent world fish market developments and medium-term projections for the period 2023-2032. Some of the key takeaways for the marine ingredients sector are listed below.

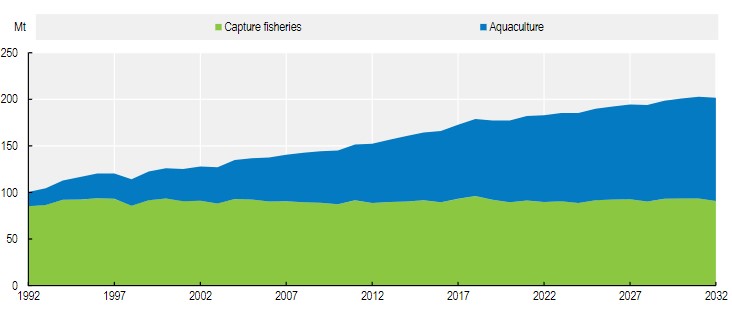

Global fish production will continue to expand to meet rising demand reaching 202 Mt by 2032, but at a slower rate than in the last decade. This slowdown in growth reflects the impact of policy changes in China, which have slowed the expansion of production, the higher costs for inputs, particularly energy, and the assumption that 2032 will be an El Niño year leading to lower production. Aquaculture will drive production growth, and is projected to account for 55% of total fish production by 2032, compared with 50% nowadays.

Figure: Aquaculture and capture fisheries production (source: OECD/FAO (2023), ”OECD-FAO Agricultural Outlook”)

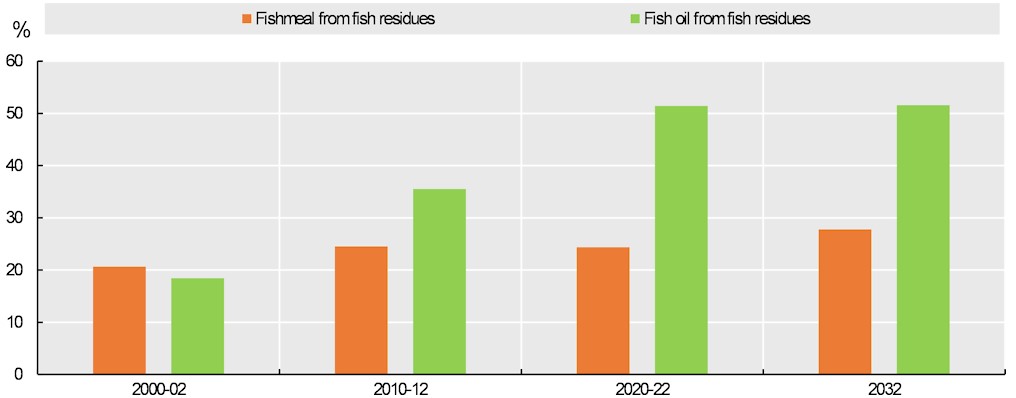

World production of fishmeal is expected to expand over the next decade, with a fluctuation of the quantity of catches of industrial fisheries for fishmeal and fish oil between lows of 15.9 Mt in El Niño years and highs of 18.3 Mt in the best fishing years. The use of fish residue and by-products is anticipated to continue, reflecting an increased capacity of the sector to utilize by-products.

Figure: Share of fishmeal and fish oil obtained from fish residues (source: OECD/FAO (2023), ”OECD-FAO Agricultural Outlook”)

In 2032, world production of fishmeal and fish oil could reach 5.4 Mt and 1.3 Mt (in product weight) respectively, which corresponds to a growth of 4.0% and 11%, compared to the base period. Markets will continue to be characterised by the traditional competition between aquaculture and livestock for fishmeal, and between aquaculture and human consumption for fish oil. A consequence of the growth of aquaculture and the reduction in fishmeal use in feed rations, due to its high price and major innovation efforts, is that oilseed meals are increasingly used to make up the shortfall in aquaculture feed. Indeed, oilseed meal use is anticipated to reach about 11.4 Mt in 2032. However, fishmeal and fish oil are expected to be used selectively at specific stages of production, such as for hatchery, brood stock and finishing diets as considered the most nutritious and most digestible ingredients for farmed fish. China will be the country utilizing the highest quantity of fishmeal as feed with a share of 42% of total consumption in 2032.

The full report can be found here.